Why Houston Suffragists Petitioned Judge Harvey

Houston suffragists scrambled in a large-scale coordinated defense in their last-chance legal hearing in Judge Harvey’s court. Texas suffragists, particularly in Houston, pursued years of legislative and legal challenges to gain the right to vote. There was one door remaining open for them in November 1920 and it was Case 91196.

“Call Goes Forth to Women of Texas to Support the Candidacy of Gov. Hobby”1

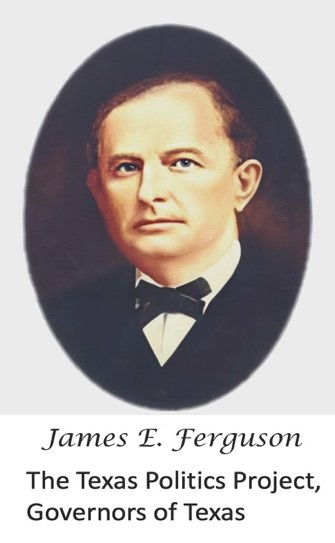

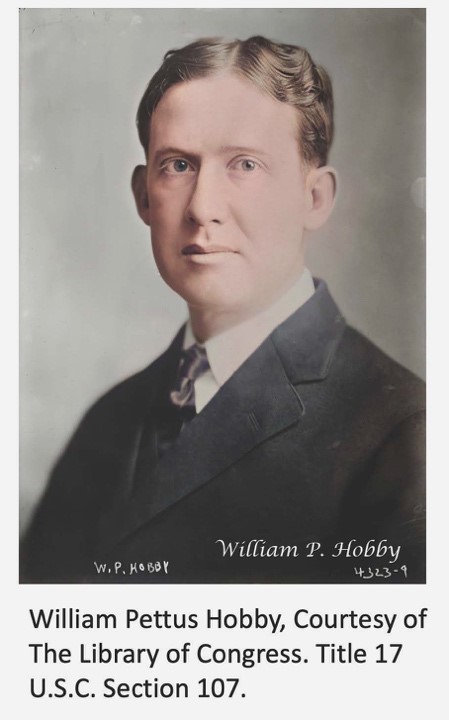

Anti-suffragist Texas Governor James Ferguson’s political allies were powerful alcohol and cotton interests that feared women’s support of prohibition and improved wages and working conditions in textile factories. When pro-suffragist Lieutenant Governor William P. Hobby assumed the governor’s position after Governor Ferguson’s impeachment in late August 1917, suffragists seized an opportunity. Texas suffragist leadership negotiated an arrangement to support Governor Hobby and his agenda if he, in turn, agreed to support woman suffrage in local and state primaries, requiring only legislative approval and no general election. The law allowing women to vote in primaries passed in the spring of 1918. Texas suffragists wanted every opportunity at any level for Texas women to vote.

Anti-suffragist Texas Governor James Ferguson’s political allies were powerful alcohol and cotton interests that feared women’s support of prohibition and improved wages and working conditions in textile factories. When pro-suffragist Lieutenant Governor William P. Hobby assumed the governor’s position after Governor Ferguson’s impeachment in late August 1917, suffragists seized an opportunity. Texas suffragist leadership negotiated an arrangement to support Governor Hobby and his agenda if he, in turn, agreed to support woman suffrage in local and state primaries, requiring only legislative approval and no general election. The law allowing women to vote in primaries passed in the spring of 1918. Texas suffragists wanted every opportunity at any level for Texas women to vote.

Governor Hobby supported amending the Texas constitution to include women as qualified voters; however, the amendment failed on June 4, 1919 with only 45.9% support.2 Three weeks later, the Texas 36th Legislature, Second Called Session, ratified the 19th Amendment to the U.S. Constitution on June 24th, 1919 (S.J.R.7). Texas became the first traditional Southern state to ratify the 19th Amendment.3 In 1918 and 1919, Texas suffragists scored two victories. They won primary voting and the ratification of the 19th Amendment, and lost one, the woman’s amendment to the Texas constitution.

“Women Now Turn Attention to Plans for Using Ballot”4

If Texas men had voted to pass the proposed June 1919 amendment to the Texas constitution including women as voters, the law would have required both sexes to pay a poll tax when the 19th Amendment went into effect on August 26th. Instead, the Texas constitution conflicted with the new federal law.  Legislators were squeezed between Texas male voters opposed to woman’s suffrage and the 19th Amendment requiring woman’s suffrage. The upcoming November election in two months gave little time for a legal solution. Governor Hobby called a special session September 21st to devise a registration process. Public interest in the legislative solution was high.5 Houston suffragists instead pinned their hopes on the “favorable opinion from Attorney General Cureton and later from the courts.”6

Legislators were squeezed between Texas male voters opposed to woman’s suffrage and the 19th Amendment requiring woman’s suffrage. The upcoming November election in two months gave little time for a legal solution. Governor Hobby called a special session September 21st to devise a registration process. Public interest in the legislative solution was high.5 Houston suffragists instead pinned their hopes on the “favorable opinion from Attorney General Cureton and later from the courts.”6

There does not seem as yet any definite plan for the bill to clear up the poll tax muddle, the attorney general’s department having held that under the state constitution no law may be passed which will require women to pay registration fee or any kind of tax because the time for the payment of such tax is from October 1 to February 1 annually. [emphasis added] Members of the legislature interviewed did not have any plan in sight to pass the measure as proposed by the governor. The attorney general’s department declares that to require a registration fee is an indirect way to collect a poll tax.7

“Hobby Asks Solons to Pass New Laws Regulating Voting”8

Governor Hobby supported free voting for women in the 1918 primary elections. He viewed women voters as a potentially large, reliable Democratic party voting bloc. He again supported allowing women to vote for free in 1920. Not all Democratic political interests shared his view. The Houston Post, an anti-suffragist leaning newspaper, wrote that allowing women and men to vote for free, would create an impossible situation in the upcoming election because there would be no registration or means to know who was actually voting.9 Clearly woman voting for free would have consequences.

The governor submitted his first message to the special session, confining his recommendations to the passage of laws governing the November election. He advocated regulations permitting women to vote without the payment of poll taxes [emphasis added] stating that the opinion of the attorney general holding that such a requirement could not be imposed on the newly enfranchised voters left no alternative in that direction … It had been held by the attorney general that in order to avoid discrimination between the sexes it would be necessary to allow both men and women to vote without the payment of poll taxes [emphasis added] … As you of course know, all male citizens of Texas are required by the constitution and laws of the State to pay a poll tax as a prerequisite for voting in the general election. In the opinion of the attorney general, all male persons who have not paid poll taxes may likewise vote in the general election [emphasis added] in November, as a result of the adoption of the nineteenth amendment … To throw the election in November wide open to every person in Texas over 21 years of age without limitation, without an official record of the name of each person voting and the payment of the customary tax whether it be a poll tax or a suffrage tax by another name, is too dangerous to think of. Yet unless there is legislation by your memorable body such will be the case …”10

The Houston Post editorial view promoted fear of “fraud” and potential voters who could “taint ballots”. “There were about 750,000 persons in Texas who qualified themselves to vote in the November election by paying poll taxes or obtaining exemption certificates. It is safe to estimate that at least 2,500,000 men and women are of voting age in Texas …”. They go on to propose a compromise, “… enact a law qualifying all of those who have paid a poll tax prior to February 1, 1920, and giving all of those who have not paid a poll tax 15 days in which to record their names and addresses at the county tax collector’s office, and pay an amount equal to the poll tax which those voters who previously qualified have paid, and thus qualifying for voting at the November election. While it would be desirable to give those voters who have not paid poll taxes a longer period of time in which to qualify, the date of holding the election prevents it.”11

The Houston Post editorial view promoted fear of “fraud” and potential voters who could “taint ballots”. “There were about 750,000 persons in Texas who qualified themselves to vote in the November election by paying poll taxes or obtaining exemption certificates. It is safe to estimate that at least 2,500,000 men and women are of voting age in Texas …”. They go on to propose a compromise, “… enact a law qualifying all of those who have paid a poll tax prior to February 1, 1920, and giving all of those who have not paid a poll tax 15 days in which to record their names and addresses at the county tax collector’s office, and pay an amount equal to the poll tax which those voters who previously qualified have paid, and thus qualifying for voting at the November election. While it would be desirable to give those voters who have not paid poll taxes a longer period of time in which to qualify, the date of holding the election prevents it.”11

“Election Law Extends Time of Poll Taxes”12

The Houston Post‘s September 22nd suggestion was similar to the special session’s solution that Governor Hobby signed after the legislature adjourned Saturday night, October 2.13 Ten days later, Attorney General Cureton’s office issued a complete description.

The new election laws simply extend to midnight October 21st, the time for the payment of poll taxes or the obtaining exemption certificates, according to ruling just issued by the attorney general’s department … the ruling states that all men and women who paid their poll taxes for 1919, are not affected by the new law in any way. Men and women who were eligible but failed to pay their poll taxes before February 1, 1920 now have until October 21 in which to pay them.” Since the 1921 poll tax payment period began on October 1, some voters were already paying the tax for 1921 elections. For those individuals, “Persons who paid their poll taxes after February 1, 1920 … must obtain a receipt … such receipt will entitle them to vote in any election between now and February 1, 1921 … the total tax remains $1.75 …14

Unfortunately, this clarification was sent out only nine days before the window closed on October 21st.

“Plan Suit to Test Women’s Poll Tax Law”15

While some women paid during the special payment window, other suffragists planned a legal challenge. Leading Houston suffragists challenged of the special session law as unconstitutional because so few Harris County women are qualifying during the poll tax payment window. Of the estimated 40,000 otherwise eligible women, few paid. The lawsuit sought an injunction against enforcement of the new state law.16

Mrs. Hortense Ward and Judge C.F. Stevens prepared the petitions to be filed in the 80th District Court. Judge Stevens said he had no doubt but that the law passed by the special session of the legislature is unconstitutional. A writ of mandamus will be asked impelling all election officers to accept the votes of women in compliance with the federal suffrage amendment.17

“First Suit Filed To Test Validity of Suffrage Act”18

Hortense Ward’s lawsuit against the poll tax wasn’t her first effort for Texas woman’s rights. Her lobbying was instrumental in passage of the “Married Woman’s Property Law” (H.B. 22), giving women the right to control their own property and money in 1913. She wrote newspaper articles and published a pamphlet encouraging hundreds of thousands of Texas women to register for the 1918 primary. She was a leader in the Texas Equal Suffrage Association and was Harris County president in the years leading up to the 19th Amendment.19

The plaintiff, Mrs. Mary Francis Hinckley, is a well-known realtor and independent businesswoman.20

The named defendant is Mr. Edward V. Ley, presiding officer of the Woodland Heights polling box, Precinct No. 2. Mr. Ley is a property developer in Woodland Heights. His wife, Cora, is a suffragist. “The action today is a friendly one as Mr. Ley told the attorneys for the applicant that he was in favor of women being permitted to vote without payment of a poll tax, and that he wanted to see the matter settled.”21

The constitutionality of the law is questioned in the action filed. The applicant holding that the constitution of Texas does not require that women shall pay the poll tax and further it provides that all poll tax payments for any year shall be made not later than January 31 of the following year. The legislature extended the time of the 1919 poll taxes until October 22 of this year.22

Should the contentions of the applicant be upheld in that the legislature was without power to extend the time for the payment of poll taxes, but other contentions be denied it will have the effect of invalidating the new law as it applies to elections to be held between now and February 1, 1921. If all contentions are upheld it will make the adoption of a constitutional amendment necessary in order to collect poll taxes from women in the future. The attorney general recently issued a ruling on the operation of the new law, and in this ruling he declined to rule on the constitutionality of the law as a whole.23

The Texas 80th District Court jurisdiction covers two counties, so Judge Harvey alternated court hearings at the Waller County Courthouse in Hempstead with hearings at the Harris County Courthouse in Houston. He agreed to travel from Hempstead to Houston to hear the Case 91196 on Saturday morning, October 23rd, nine days before the November election.

“Harvey Holds New Poll Tax Law Invalid”24

There was an immediate announcement after the short hearing. Judge Harvey declared the poll tax law enacted by the special session unconstitutional.

The law attempting to impose on women a poll tax prerequisite to their voting in the next general election to be held next month or in any other election held during the current year is void and women have the right to vote in all such elections without payment of a poll tax … Judge Harvey’s decision will affect the women voters of Waller County also … and according to Mrs. Ward the precedent by this decision probably will control the action of many election officers throughout the state.25

“Decision May Allow 80,000 to Vote Here”26

Judge Harvey’s decision strengthened the argument that because the 19th Amendment prohibits discrimination on the basis of sex, men as well as women can vote for free.

Many Houston lawyers hold that if women can vote without a poll tax, so can men… Election officials are worrying their brains over knotty questions that may arise at the polls as the result of having voters who have not even registered. It is said safeguards will be taken against “repeating”.27

“Judge Harvey’s Opinion”28

Judge Harvey’s careful explanation was printed in The Houston Chronicle:

A poll tax is a debt and is a charge against and collectable from the property of the person against whom same is laid. Our constitution prohibits the making of a retroactive law. A retroactive law is one made to affect acts or transactions or considerations already accrued, and which imparts to them characteristics or ascribes to them affects which were not inherent in their nature in contemplation of the law as it stood at the time of their occurrence. It gives a right or imposes a liability on a past status where none before existed. On the first day of January A.D. 1919, nor at any time before the passage of the law in question was a poll tax laid against a woman either by the constitution or statute. Therefore it is obvious that the law in question which undertakes after February 1, 1920, to lay a poll tax against women on January 1, 1920 or any previous year and thereby charge her with a debt to the state and render her liable therefore imposes a new liability in respect to transactions already past and is therefore void under the constitutional prohibition against retroactive laws. Being void such law imposes no legal obligation on women and because the tax sought to be imposed is not a legal tax, is equivalent to no tax at all.29

“Can’t Affect Right to Vote”30

But even though it be conceded for the sake of argument that the poll tax sought to be laid against women by the law is valid as a tax and creates a lawful debt against her. It by no means follows that her failure to pay same will affect her rights as a voter. By the amendment to the federal

constitution adopted during the current year every woman in the estate having the qualifications prescribed by our state constitution except as to sex is made a qualified voter for the first time. This being a constitutional right it cannot be abridged or impaired nor can any pecuniary burden be lawfully imposed [emphasis added] as a price of its exercise the elective franchise is stated in the constitution as follows: That any voter who is subject to pay a poll tax under the laws of the State of Texas shall have paid said tax before he offers to vote and hold a receipt showing his poll tax paid before the first day of February next preceding such election.31

“Why Poll Tax Does Not Apply”32

It is plainly apparent therefore that a poll tax that is not laid or does not exist before the first day of February next before the election at which the voter offers to vote not be paid before that date and is therefore not the burden or tax meant to be made conditional to the exercise of the constitutional rights of a voter. By the express language of the constitution above quoted it is clear that the condition which defeats the exercise of the elective franchise is composed of two elements-namely (1) the voter must be subject to the payment of a poll tax lawfully imposed on him before the first day of February next preceding the election at which he offers to vote, and (2) that he shall have paid same before that date. [emphasis added] Any condition relative to the payment of a poll tax by a voter which does not possess these two elements is not authorized by the constitution and is void. It is impossible for woman to pay before the first day of last February the poll tax attempted to be imposed on her by the law in question because the law was passed after that date and the legislature is not allowed to attach a condition to the elective franchise which is impossible of performance. Neither can a pecuniary obligation be imposed as a condition to the exercise of the constitutional right to vote unless it clearly comes within the scope and meaning of that allowed by the constitution which the poll tax provision in question obviously does not do. Therefore the law attempting to impose on women a poll tax as a prerequisite of their voting in the general election to be held next month or in any other election held during the current year is void and women have the constitutional right to vote in all such elections without the payment of a poll tax. [emphasis added].33

![]()

Since Attorney General Cureton’s opinion that Judge Harvey’s ruling only applied to Waller and Harris Counties, suffragists in other jurisdictions needed to bring similar lawsuits in their areas if they wanted to vote without paying a poll tax. Texas had 82 districts and there was no time. Also, there was no time to bring Case 91196 before an appeals court that might rule statewide the poll tax was unconstitutional. Attorney General Cureton declined to make an opinion as to the constitutionality of the special session woman’s election law.34

“Determined Opposition by Suffragists”35

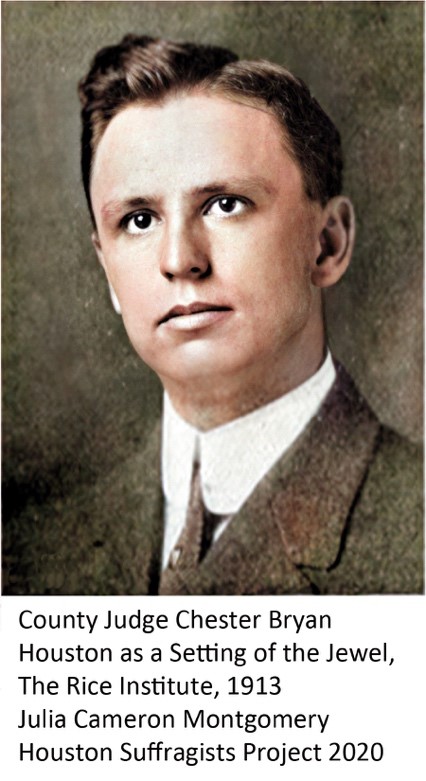

Mrs. Ward had her first intimation that election judges planned to turn women away from the polls when she overheard a conversation of an election judge. When the Harris County election board’s plan became public, Mrs. Ward‘s publicly “… issued a warning to the election board and election officials … that any attempt to disfranchise the women November 2nd will lead to charges of contempt of court and violation of the federal election law being filed against them … County Judge Chester H. Bryan a member of the election board when asked Saturday about the rumor refused to make denial “She has recourse to law.”36

Mrs. Ward had her first intimation that election judges planned to turn women away from the polls when she overheard a conversation of an election judge. When the Harris County election board’s plan became public, Mrs. Ward‘s publicly “… issued a warning to the election board and election officials … that any attempt to disfranchise the women November 2nd will lead to charges of contempt of court and violation of the federal election law being filed against them … County Judge Chester H. Bryan a member of the election board when asked Saturday about the rumor refused to make denial “She has recourse to law.”36

This development virtually on the eve of an election already fraught with possibilities, came like a bombshell in local political circles yesterday. If carried to a conclusion the opposition to Judge Harvey’s decision will furnish some of the hottest political fireworks Harris County has ever seen. Contempt proceedings against any election officer disobeying the court order were predicted by attorneys who filed the suit on which the mandamus was granted.37

“Battle Over Poll Tax is at an End”38

As predicted on the following day, Judge Harvey’s courtroom was packed with suffragists and their attorneys. On this day, instead of Mrs. Hinckley as the sole plaintiff of Case 91196, she was accompanied by 12 additional plaintiffs including men.

The court order was made on a new suit filed by eight Harris County women after they discovered that the Harris County election board through County Judge Bryan, chairman had issued instructions by letter to every presiding officer advising them to permit no one to vote without a poll tax receipt … The court’s order Monday, however supersedes our instructions” Judge Bryan added, “We have done all we can.39

“Qualifications for Men”40

Meanwhile Judge Harvey, Judge Bryan and United States District Attorney D. E. Simmons were being bombarded with questions in regard to who can vote. It was generally understood no man would be allowed to vote without holding a poll tax receipt unless he be a discharged soldier. Election officials have prepared for the heaviest vote ever cast at a general election in this county. The polls will open at 8 a.m. and close at 7 p.m. County Clerk Albert Townsend announces …41

“Decision Not Binding”42

Judge Bryan comments to the press about his view as Harris County Judge.

The decision of Judge Harvey which has been so much discussed, is, in our opinion and according to legal advice obtained by us, not binding upon the presiding officers of election. The original defendant named in that suit is not, and was not a presiding officer of election; and we are reliably informed that the persons who instituted said suit had knowledge of that fact before the suit was filed. We are advised that the injunction or mandamus issued in that case is binding on no one but E.V. Ley, the original defendant … Our instructions to the election officers has been prompted, not alone by a desire to see the law upheld as it now exists, but further to meet and anticipate a concerted effort upon the part of leaders and supporters of their political parties to urge persons of all races and color, both male and female, to go to the polls and vote, whether they have paid a poll tax or not. It can readily be seen that such condition will furnish abundant opportunity for “repeating” or frequent voting by the same persons, as without the poll tax requisite there will be no means of identifying a voter, or the number of times he or she has voted. This was the evil that the legislature sought to provide against.43

“Urges Negroes to Vote”44

A newspaper published by and circulated among the negro race has already published an issue with an appeal to both sexes of said race, on the front page under the headlines, “All men and women above 21 years of age can vote without a poll tax” and urging every negro woman and every negro man to go to the polls and because of such ruling, demand the right to vote without payment of poll tax … Judge Harvey said Monday that he had no knowledge of any person attempting to disobey his new injunction. Should any occur, however, it was considered certain that contempt proceedings would be instituted.45

“Plaintiffs in Suit”46

“The plaintiffs in the suit filed Monday are Mrs. Eunice Ralls, Mrs. Ida Buvinghausen, joined by her husband, William Buvinghausen; Mrs. May Tally and her husband, L.H. Tally; Mrs. Mary F. Hinckley and husband E.G. Hinckley; Mrs. Jennie Marsac and husband, S.L. Marsac; Mrs. Katie Bailey, Mrs. O.D. Shuptrine and Mrs. R.G. Alexius. Women opposing the contemplated action of the election board were busy Sunday circulating resolutions protesting against the move. The women who signed the resolutions represented 12 or more local organizations.”47

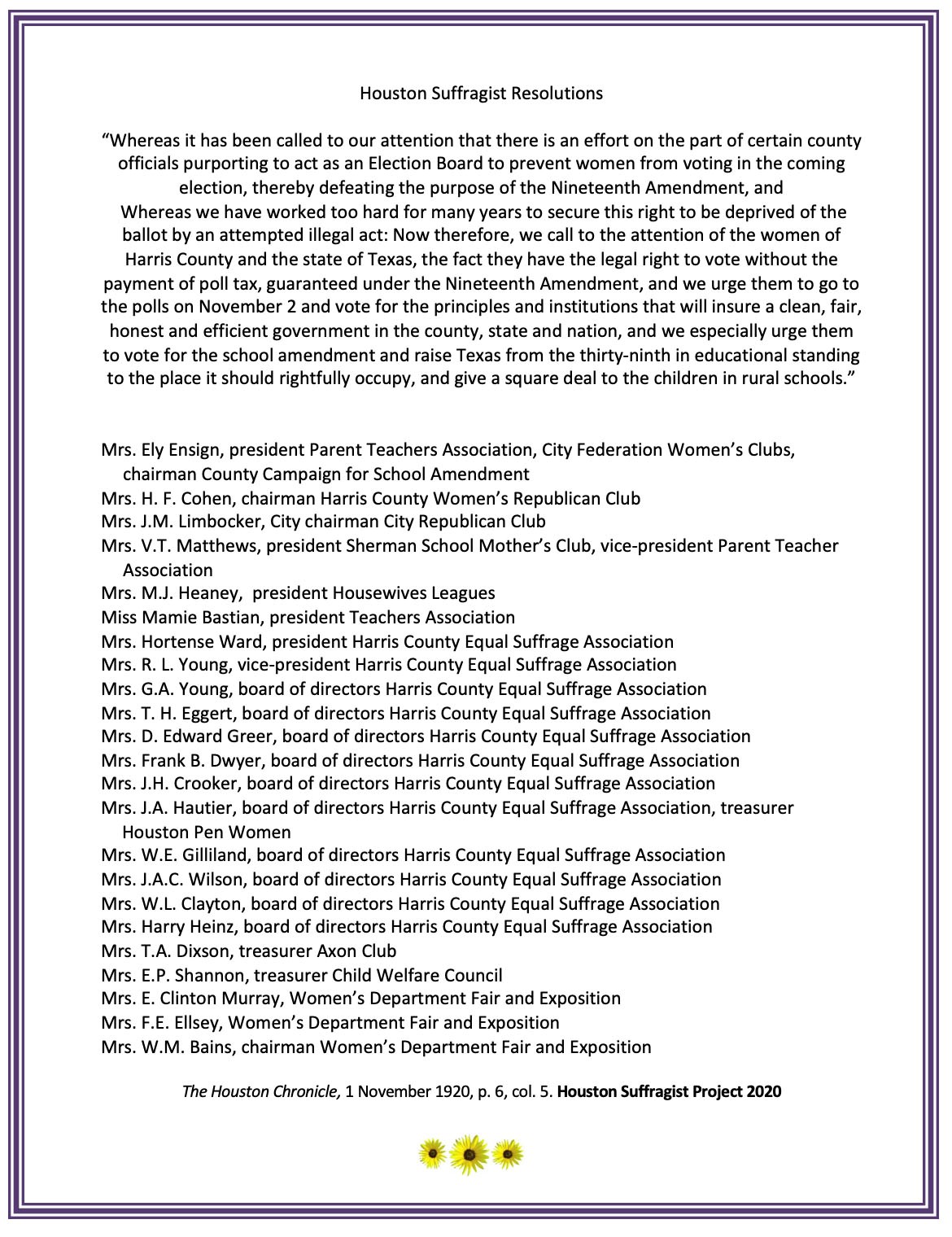

“Resolutions Adopted”48

“Call Goes Forth to Women of Texas to Support the Candidacy of Gov. Hobby,” The Houston Chronicle, 26 May 1918, p. 13, col. 3. Mrs. Hortense Ward’s open letter describing the Texas suffrage work to bring women to the point of obtaining the right to vote in Texas primaries. She also presents the case for women to vote for Governor Hobby.↩︎

“Amendments to the Texas Constitution Since 1876, Current Through the November 5, 2019, Constitutional Amendment Election” Texas Legislative Council, February 2020, https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&ved=2ahUKEwiEzPHyu6rrAhUPbKwKHb5pD0UQFjAAegQIBBAB&url=https%3A%2F%2Ftlc.texas.gov%2Fdocs%2Famendments%2FConstamend1876.pdf&usg=AOvVaw3lmG-iH1f20lplwYawAQV7↩︎

19th Amendment Ratification Fact Sheet – Women’s History, National Archives, https://www.archives.gov/files/exhibits/nates/files/19th-amendment-ratification-fact-sheet.pdfhttps://www.nps.gov/subjects/womenshistory/19th-amendment-by-state.htm↩︎

“Women Now Turn Attention to Plans for Using Ballot,” The Houston Chronicle, 19 August 1920, p. 13, col. 4.↩︎

“Members Hope Extra Session will be Brief,” The Houston Chronicle, 21 September 1920, p. 14, col. 1.↩︎

“Women Now Turn Attention to Plans for Using Ballot,” The Houston Chronicle, 19 August 1920, p. 13, col. 4.↩︎

“Members Hope Extra Session will be Brief,” The Houston Chronicle, 21 September 1920, p. 14, col. 1.↩︎

“Hobby Asks Solons to Pass New Laws Regulating Voting,” The Houston Post, 22 September 1920, p.1, col.1.↩︎

Ibid.↩︎

Ibid.↩︎

Ibid.↩︎

“Election Law Extends Time of Poll Taxes Attorney General’s ruling Holds All Who have not Qualified May Do so by Paying Before October 21,” The Houston Chronicle, 12 October, 1920, p. 7, col. 1.↩︎

“Governor Signs New Laws Passed at Extra Session,” The Houston Chronicle, 4 October 1920, p. 1, col. ↩︎

“Election Law Extends Time of Poll Taxes Attorney General’s ruling Holds All Who have not Qualified May Do so by Paying Before October 21,” The Houston Chronicle, 12 October, 1920, p. 7, col. 1.↩︎

“Plan Suit to Test Women’s Poll Tax Law,” The Houston Chronicle, 17 October 1920, p. 1., col. 6.↩︎

Ibid. See also “39,800 Women of Harris County Do Not Qualify to Vote,” The Houston Post, 15 October 1920, p. 12, col. 3.↩︎

“Suits Prepared to Test Validity of Suffrage Law,” The Houston Post, 19 October 1920, p. 4, col. 1.↩︎

Ibid.↩︎

“Legislature Has Power to Grant Women Ballot, Interesting Opinion is Given by Judge Ocie Speer With Reference to Primary Elections. Houston Suffragists Expect Governor Hobby to Submit such Legislation at Special Session,” The Houston Chronicle, 17 February 1918, p. 6. Col. 3., See also “Suffrage Leaders Go to Austin to Urge the Enfranchising of Women,” The Houston Chronicle, 24 February 1918, p. 5, col. 2.↩︎

“First Suit filed to Test Validity of Suffrage Act,” The Houston Post, 20 October 1920, p. 9, col.1.↩︎

Ibid.↩︎

Ibid.↩︎

“Suit to Test Suffrage Law is Instituted Friendly Mandamus Proceedings Brought in Eightieth Court Against Woodland Heights Presiding Officer,” The Houston Chronicle, 19 October 1920, p.1. See also “Poll Tax Mandamus Set for Saturday,” The Houston Chronicle, 21 October 1920, p. 1, col. 1.↩︎

“Harvey Holds New Poll Tax law Invalid, Decision Will Permit Women to Vote in General Election of November 2 Without Poll Tax,” The Houston Chronicle, 23 October 1920, p. 1, col. 7.↩︎

Ibid. See also “Judge says Women Can Vote Without Paying Poll Tax, Law Recently Passed by the Legislature is Void, Is Court Ruling, 40,000 Women Enfranchised, Decision Grew Out of Suit Filed Against Presiding Officer of Precinct 2,” The Houston Post, 24 October 1920, p. 1 col. 3.↩︎

“Decision May Allow 80,000 To Vote Here, Many Houston Lawyers Contend if Women can Vote Without a Poll Tax Receipt So Can Men,” The Houston Chronicle, 24 October 1920, p. 48, col. 5. See also “Judge Harvey’s Decision No Surprise at Austin,” The Houston Post, 24 October 1920, p. 48, col. 5.↩︎

Ibid.↩︎

Ibid.↩︎

Ibid.↩︎

Ibid.↩︎

Ibid.↩︎

“Decision May Allow 80,000 To Vote Here, Many Houston Lawyers Contend if Women can Vote Without a Poll Tax Receipt So Can Men,” The Houston Chronicle, 24 October 1920, p. 48, col. 6.↩︎

Ibid.↩︎

“Attorney General Says Follow Court Ruling,” The Houston Post, 30 October 1920, p 14, col.1. See also “Largest Vote in county’s History Expected Tuesday Mandamus Order will Allow All Women to Vote,” The Houston Post, 30 October 1920, p. 14, col. 1.↩︎

“Plan to Bar Women From Polls Despite Ruling of Judge Harvey Arouses Determined Opposition Suffragists Issue Warning that Due Course of Law Will Be Followed,” The Houston Post, 31 October 1920, p. 1, col. 5.↩︎

Ibid.↩︎

“May Defy order Permitting All Women to Vote Contempt Proceedings Are threatened if Election Officers Fail to Carry Out Court’s Decision,” The Houston Chronicle, 31 October 1920, p. 1, col. 5.↩︎

“Battle Over Poll Tax is at an End, Judge Harvey Issues Mandamus Order to election Officials to Permit Women to Vote” “Done All We Can,” Says Bryan; “Court Order Supersedes” Instructions Issued to Judge.” The Houston Chronicle, 1 November 1920, p.1, col. 1.↩︎

Ibid.↩︎

Ibid.↩︎

Ibid.↩︎

“Battle Over Poll Tax is at an End,” (continued from page 1.) The Houston Chronicle, 1 November 1920, p. 6, col. 3.↩︎

Ibid.↩︎

Ibid.↩︎

Ibid.↩︎

“Battle Over Poll Tax is at an End,“(continued from page 1.) The Houston Chronicle, 1 November 1920, p. 6, col. 4.↩︎

Ibid.↩︎

“Battle Over Poll Tax is at an End,“(continued from page 1.) The Houston Chronicle, 1 November 1920, p. 6, col. 5.↩︎